47. Ten Common Startup Fundraising Mistakes and How to Avoid Them

As a Global Entrepreneur in Residence at the Founder Institute https://fi.co and chair of the selection committee for the North Bay Angels https://www.northbayangels.com/ I see heaps of pitches. Unfortunately, the same few fundraising mistakes doom most of their efforts. I want to share with you my list of the ten most common fundraising mistakes founders make and how you can avoid them.

Reality Check

Watch this blog on YouTube

Most companies are not a good fit for angel or VC investment. Only companies with the potential for explosive growth and a clear exit make financial sense for those kinds of investors. Incredibly successful companies in businesses like construction, plumbing, retail, and restaurants would still not be appropriate because they don't fit those requirements.

For the rest of this discussion, I will assume that your company is a venture investable business. On to the mistakes:

1 – Only Looking at Equity

Just because you can get angel or VC investment does not mean that you should. Some other sources of growth capital don't require selling part of your business.

First, you can look for grants from the government or other organizations. This option typically applies to companies that create some public benefit. Many grants fund medical and green-tech startups, but almost any company might be able to get in on the action. The great advantage of grants is you don't give away ownership, and you don't need to pay it back. On the downside, they often come with requirements for how you use the money and licenses to any intellectual property you develop.

Second, you can leverage partnerships to pay for your product development. If a bigger company needs to leverage the solution you are creating, they may pay you to make it. In return, they might ask for exclusivity, discounts, or other non-equity compensation. These partner funders often become significant customers, or even acquirers, down the road.

Third, you might be able to use debt to fund your cash needs, particularly over the short term. Some individuals and institutions will lend you money to finance the production of your product or to cover costs while you wait for customers to pay their bills. Venture debt provides another funding source for companies with significant traction. It generally requires issuing warrants to the lender but gives away much less equity than a conventional investment.

Fourth, you could forgo fundraising entirely and opt to bootstrap your business. If you can generate some revenue quickly, you may be able to leverage that into the growth you need. This is only viable if the competitive environment does not necessitate explosive growth.

In reality, most companies do some, if not all, of these things at some point.

2 – Going in Cold

At the North Bay Angels, companies introduced by a member receive funding several times as often as previously unknown startups. You are at a massive disadvantage if your first interaction with an investor is to put your hand out asking for money.

Start networking as early as possible. Leverage your existing connections and relationships to get introductions to potential investors or to people who can make those introductions. Ask them for advice or information. Most investors love helping founders and will be happy to give a little bit of time and attention. Follow up with them with information on your progress. When the time comes to raise your next round, you will have a whole stable of angels or VCs that know you, know your company, and feel warmly towards you.

3 – Fundraising too Early

A large fraction of companies applying to the North Bay Angels are not ready for angel investment. Unfortunately, you typically only get one bite at that apple. Ask investors if they think you are ready when you are doing your pre-fundraising networking. What benchmarks or metrics do they need you to hit before applying?

Most companies are "too early" because they have not done the necessary validation work to reduce investment risk. We all know that investing in early-stage companies is absurdly risky, but unnecessary risk is unacceptable. Before you apply, make sure you have examined all the key assumptions underlying your business model. Do your unit economics work at scale? Will customers change behaviors to adopt your solution? Can you acquire customers at a reasonable CAC? Traction is the best way to prove most of these, but if you can't get that without funding, find other ways of gathering data or running experiments. Then, before you apply, get outside confirmation that you are ready. It is easy to believe your hype.

4 – Missing the What and Why

I often reach the end of a pitch, having heard all kinds of information but with no idea what the company does or why. I need to be able to picture your business in action and your users interacting with the solution. Give some specific examples of the problem, rather than stating it abstractly. Saying that you improve process efficiencies does not paint a clear picture. Tell me about what users had to do before, that they don't need to do after adopting your solution.

It may help to think about this visually. Cinematographers usually open with a wide establishing shot, telling the viewer where things are happing and generally what is going on. Then they can move in with tighter shots to focus on specific details. You need to make sure I understand that context before I can follow you down into the weeds.

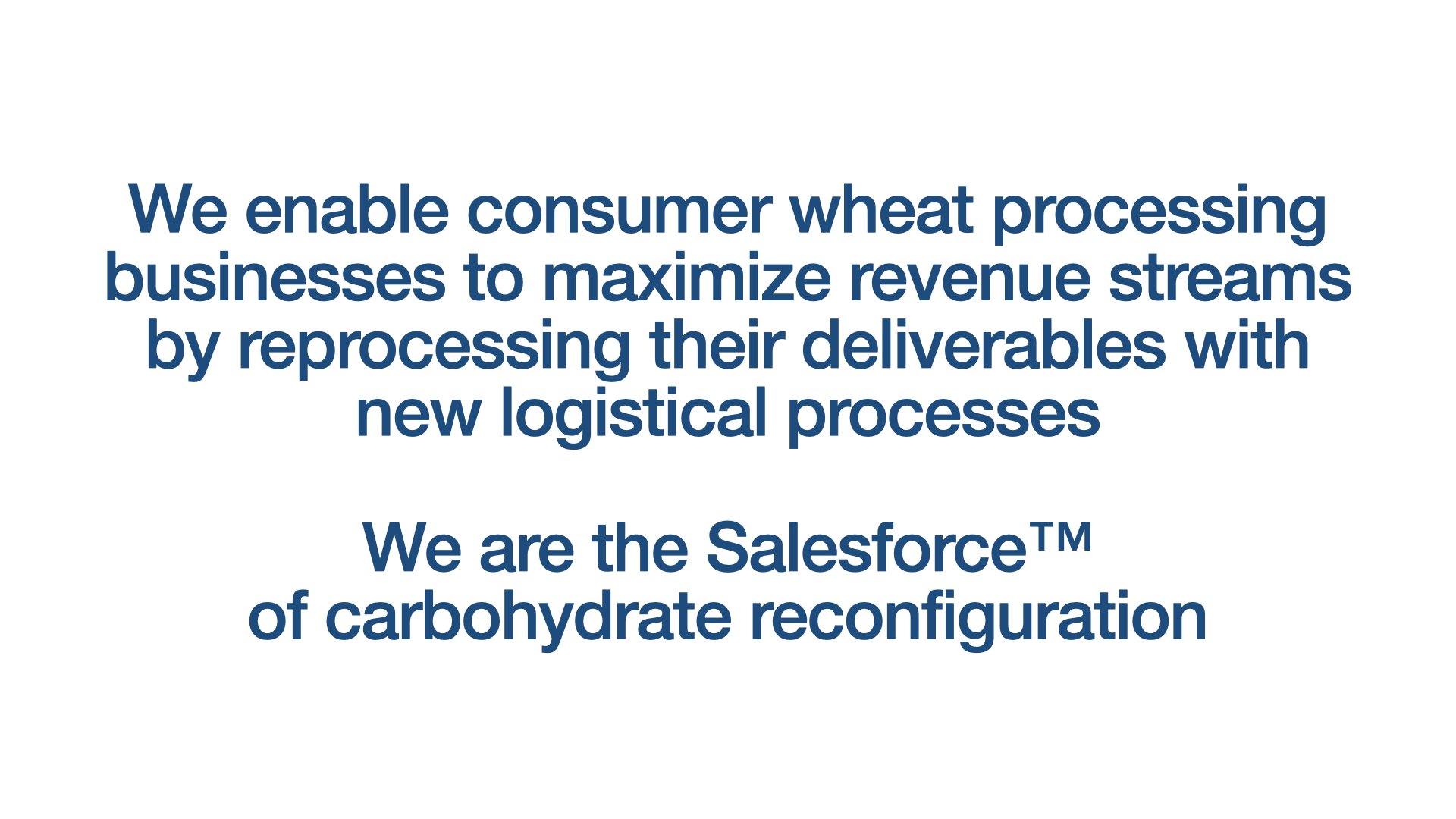

Often the founder's description of their company is too confusing or abstract to orient me. The founder will open their presentation with something like this:

That statement transmits almost no useful information into my brain. Instead, the founder could have said something much more straightforward and direct like:

5 – Failing to Understand Your Audience

You know your business far too well, or at least I hope you do. You no longer remember what was obvious about your market space and what you learned while working on your business. This leads founders, particularly technical founders, to assume that their audience of investors understands these things too. I assure you that we do not.

Additionally, we are not interested in the same things as you or your customers. You care about running the company. Customers care about solving a problem. We care about your company thriving and returning many times our investment. Here are four guidelines to help you connect when talking with investors:

Use standard everyday English and avoid jargon, technical terms, or acronyms. It is vital that the investor be able to immediately comprehend what you are saying. If they are confused, they will move on to the next company.

Talk about your business, not about the technology. I want to know that your company makes sense. How will you get customers? What key metrics are important?

Focus on benefits rather than features. This seems to be a pervasive problem in competitive matrix slides. Don't tell me that your starship uses a freem-drive; tell me what using a freem-drive enables that your competitors can't provide.

Finally, this is a pitch, so you don't have much time. Just skim the surface rather than wallowing in the details. If you are saying interesting things, we will want to go deeper in the next conversation.

6 – Weak Communications

In a perfect world, investors would judge your company solely on the quality of your idea, plan, and execution. Unfortunately, we don't live in that world. Investors are unlikely to see past an ugly surface to the gold within.

All aspects of your communications must be clear and on-point. Fundraising is an incredibly competitive business. There are vast numbers of startups chasing limited funding dollars. Your enthusiasm and energy need to shine through in every interaction, even in writing. Be visibly excited about your business. If you are not super passionate about the business opportunity, why should anyone else get excited? You don't want to take it to an absurd extreme, but you probably need to be more energetic than you usually are. If you are an introverted engineer, that would be a whole lot more energetic than you typically are.

Wherever possible, use stories and narrative to convey information. Stories are more powerful than facts. Humans both understand and remember stories far more than data points. Steve Jobs was a master of this. In the launch keynote for the MacBook Air, he could have talked about its dimensions, but instead, he described how it fitted in an envelope. Every article on the event wrote about that example. It was so impactful that I am still talking about it many years later.

Aesthetics matter. You, your deck, your handouts, your website, all need to look good. A sloppy deck, or poor personal grooming, taints our impression of everything else. We are likely to wonder if you can't create something as relatively simple as an attractive PowerPoint deck, should I trust you to manage the complexities of a startup company? Conversely, when you look like you have total mastery over the "little things," it suggests you know how to ensure quality results. People might not have that as a conscious reaction, but unconsciously this can poison the investors' entire perception of your startup.

Finally, you need to master your presentations. Practice your pitch dozens of times, both by yourself and with a critical audience. If you can stand it, record a video of your pitches so you can analyze every cringe-inducing error. You can't look effortless unless you have put in the work. Additionally, it is hard to adapt on the fly to your audience's reactions, questions, and interruptions, unless you know the presentation well enough to deliver while focusing on other things.

7 – Hiding Weaknesses

Many startups have some skeletons in the closet. Perhaps past co-founder issues, down rounds, or pivots. Maybe you don't have strong intellectual property protections, or you built most of your solution using third party components. You don't need to shout these drawbacks from the rooftops, but don't make me find them while deep in due diligence either. If it looks like you have been trying to keep these issues hidden, you are violating our trust. And trust is everything in early-stage investing.

Angels have very little power once they write their checks. We need to believe that the founders will continue to act with integrity and their investors' best interests at heart. Anything that throws doubt on that trust can kill a deal.

8 – Failing to Make Commitments

Often founders are vague about timelines and milestones. Their "use of funds slide" talks about what they will spend the money on, but not what that will deliver. I want to know that after this investment, you will release a new version of the product with the following enhancements, grow to some number of customers, and generate a specific amount of revenue. Those achievements should also tie to the milestones you need to hit before the next round of financing. You need to show that you will be able to raise that next round at a high valuation because of the accomplishments we are funding.

If you can show a history of making and keeping commitments, even better. Don't worry; we understand that the startup world is chaotic and that most of your projections are hardly better than wild ass guesses. However, we want to understand your intentions and expectations. Clearly articulated commitments and milestones give confidence that you have thought through your strategy and understand how to go forward towards your long-term goals.

9 – Raising too Much (or too Little) Capital

Sometimes funding applications draw an immediate rejection because they are raising too much money or too little. Asking for too much raises some concerns. If you are raising a big round, but the valuation is modest, I worry that you will get so diluted that you will lose motivation. I don't want to own the whole company and have you feel like an employee. I want you chasing a big carrot over the next several years of intense work.

Alternatively, a big ask without significant dilution means high valuations. The higher the price I pay now, the lower the return I get later. Simple. Since I know that most of my angel investments will fail, that potential return needs to be very high. If your valuation is out of line, I probably have other companies with a similar chance of success that could deliver better returns.

More commonly, I see founders asking for too little money. They are trying to raise something like twenty-five thousand dollars. A tiny investment won't get the company to the next critical milestone. I suspect this happens because the founder lacks confidence or that they were rejected when asking for more. They hope that "dropping the price" will make the sale easier. Either way, it makes them look inexperienced and unready. Your raise should take you to the next significant milestone and several months beyond. You need padding for when your development takes longer than expected and when the next investment round takes longer as well. Both are likely. If you run out of cash, you will be over a barrel. Either the company will fail, or you will suffer a down round that crushes both of our ownership percentages.

10 – Failing to Follow-up

Finally, follow-up after your introduction, pitch, and any other interaction. Most investors are busy and easily distracted. If you wait a few days to get back to us or set the next meeting following a pitch, I am likely to have forgotten most of what you said and be off chasing some new shiny object. If possible, set your next meeting during the current one. Set a date in advance for due diligence calls within a couple of days of pitching an angel group.

Then keep following up and staying in touch. If they will let you, get everyone on a regular update mailing list. Stay front of mind and help us remember who you are and what you are doing. In those updates, make commitments and show that you are hitting them, ask for help, and crow about accomplishments. Even after a rejection, this kind of ongoing interaction can keep the relationship warm and allow you to ask again in the future, perhaps with better results.

Conclusion

Fundraising is hard, time-consuming work. Even if you do everything right, the odds of any angel or VC investing in your company are low. But, if you make these unforced errors, the odds quickly drop to zero. You are taking a huge risk as an entrepreneur. Make sure you give yourself the best possible chance of success.

You can also subscribe to Feel the Boot as a podcast or listen immediately below.